By Yaw Owusu-Boahen | March 2026

In August 2025, we launched Cash Catalyst, the first “Accelerated Baby Bonds” program in the country. The program combines capital, financial education, and wraparound services to measurably increase wealth for 52 young adult residents of Greater New Haven. We structured Cash Catalyst to mirror Connecticut’s first-in-the-nation Baby Bonds law, using the Connecticut Treasurer’s requirements for participation and distribution. Like Connecticut’s law, we selected low-income participants between ages 18 and 30 and informed them of their eligibility along with the distribution restrictions.

They can use their Baby Bonds to purchase a home, start a business, invest in retirement, or pursue an accredited job training or university. To fulfill the financial education requirement for distribution, we provided participants with customized MoneyByrd courses as well as six virtual Wealth Workshops.

We designed a self-directed distribution process, with participants required to complete an “investment memo” and meet with an Edward Jones financial advisor before funds would be transferred directly to the validated wealth-building institution. For example, participants wishing to use their “Baby Bond” as part of a down payment on a home would request that their funds be sent to their preferred mortgage lender.

Our goal was not simply to distribute capital, but to test whether Baby Bonds can function as intended when layered onto the real financial lives of low-income young adults. We aimed to bring Connecticut’s mandated infrastructure to life so that we could identify critical gaps and organize wraparound services into “must-haves” and “nice-to-haves.”

Seven months later, we have identified a core tension that no wraparound service can truly remedy: many of the people this policy is designed to serve are too financially unstable to make the most of this opportunity. As a case in point, we can confidently secure up to $50,000 of down payment assistance for any participant in our program, but we cannot confidently secure a mortgage for the remainder of the house purchase price. How is this possible?

The answer lies in our participants’ balance sheets.

Our 52 Cash Catalyst participants are majority Black and Hispanic young adults of Greater New Haven. They came to us through trusted community partners, including social services organizations, workforce development programs, and our local housing authority. As a result, participants represent a wide range of educational attainment and employment outcomes. One participant has a full-time job at a biotech company and lives independently. Another lives between residences, occasionally experiencing homelessness as she juggles caring for her infant with attending classes at a local community college.

Most of our participants are employed, with nearly 70% indicating that they worked more than six months in the previous year. However, the vast majority have not completed a higher education degree. While only three participants hold an associate’s or bachelor’s degree, 25% of our participants hold some sort of professional license or certificate.

In partnership with Urban Institute, our Cash Catalyst theory of change states that healthy balance sheets are necessary for wealth-building. Healthy balance sheets feature debt-to-income ratios under 40%, ensuring that the majority of earned income is not taken by debt service. They also feature at least three months of liquid savings, ensuring that assets would not need to be liquidated in a crisis and providing the psychological safety necessary to take on risk.

However, across all educational attainment and employment outcomes, our participants share one thing in common: strained balance sheets. The median Cash Catalyst participant holds less than $1,000 in total assets, with $10,000 of outstanding debts. 90% earn less than $50,000 per year, resulting in median debt-to-income ratios of 60%. This means that for every $1 that a median participant earns, they must commit $0.60 to paying off debt. Of the 50% of participants who knew their credit score at program start, 80% of them reported scores below 660.

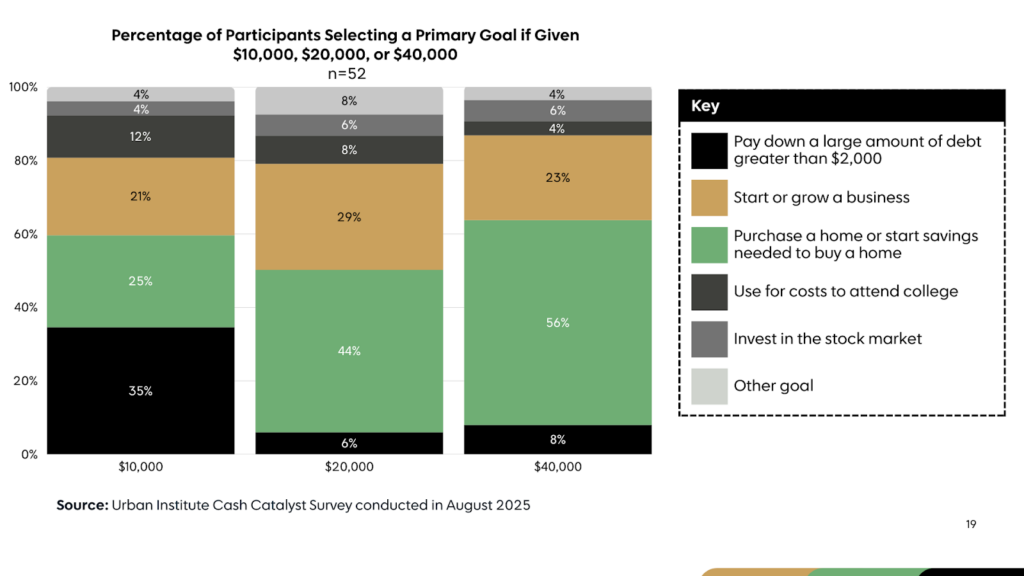

This paints a stark picture when considering the wealth-building paths most popular among Cash Catalyst participants. When asked what their primary goal would be with $20,000, 75% elected to start a business or purchase a home. Both options require much more than $20,000, meaning participants must secure sizable small business or mortgage loans, often with sub-600 credit scores.

Connecticut Baby Bonds are invested similarly to the state pensions in a fund projected to grow at 6.9% per year. If our sole goal is to maximize wealth for our participants, as responsible wealth managers, we would not recommend reallocating that capital unless that reallocation returns more than 6.9% per year on a risk-adjusted basis.

For low-income young adults in Connecticut, most businesses they can start or homes they can purchase would not clear that threshold. Timing the housing market or starting a promising business venture offers the chance for higher returns, but the risk of default is so high that reallocation would be unwise. Until a healthy balance sheet is established, the correct wealth-building choice will likely be to keep capital in a diversified market portfolio.

Generating wealth through homeownership requires much more than saving for the down payment and consistently paying the mortgage. It also requires paying annual property tax and maintenance costs, which in New Haven combine for 3-5% of the purchase price annually. With the median New Haven home priced at approximately $300,000, participants who purchase the median home would need to pay an additional up to $15,000 on top of their mortgage every year. For many of our Cash Catalyst participants, $15,000 is more than their total income in 2025.

As an entrepreneur who has advised dozens of underrepresented business owners, I’ve seen firsthand that generating wealth from a business is immensely challenging mentally, physically, and financially. 50% of new businesses fail within the first five years, often leaving business owners responsible for outstanding debt after forfeiting the collateral used to secure startup loans. In practice, that means if a participant uses their $20,000 to start their dream coffee shop and the business fails, they don’t just lose the $20,000 investment. They may also lose the house or car pledged as collateral.

This reality forces difficult but necessary questions: What does wealth-building mean when the financial foundation is unstable? And should we adjust the policy to fit present realities, or adjust those realities to better fit the policy’s aspirations? We can adjust the policy to fit current realities by modifying restrictions to support participants in first establishing healthy balance sheets. This could include permitting the use of Baby Bonds to eliminate high-interest debt, reduce debt-to-income ratios, and increase savings capacity.

We can also adjust reality to better fit the policy by building the infrastructure that enables low-income youth to establish healthy balance sheets before age 18. This could include fully-funded financial management courses offered to the least-resourced school districts, complete with financial coaches who help high school students open bank accounts and maintain low-limit credit cards to ensure good credit upon graduation. Our peers in St. Louis and Atlanta are demonstrating what it looks like to adequately prepare Baby Bond recipients, working with them years before they turn 18 to establish a healthy financial foundation.

At the Wealth Accelerator, we are attempting to adjust reality within the constraints of existing Connecticut guidelines. This includes hiring a new program manager to provide more one-on-one support for our participants as they make their allocation decisions. It includes offering free credit counseling and assisting participants as they seek higher-paying employment opportunities.

Wealth-building is difficult even for wealthy families, so wealth-building for low-income residents was never going to be easy. Cash Catalyst is showing us that it will be even more difficult than we thought.

But we are more than up to the task.

—

Yaw Owusu-Boahen is a catalytic impact investor working to close the wealth gap through investments in people, place, and platforms. Currently, the Executive Director of Wealth Accelerator CT and VP of Impact Investing at ConnCORP, Owusu-Boahen, launches wealth-building solutions for low and moderate-income families in Connecticut.